Single Family Acquisition Analysis: Case Study

Introduction:

In March 2020, 15% of homebuyers in the United States were investors. By June 2023, that figure had risen to 26%, reflecting a significant shift in the real estate landscape as more individuals and institutions sought to capitalize on the unique opportunities created by the pandemic. During the early days of COVID-19, nationwide shutdowns brought new developments and home sales to a halt, creating uncertainty and fear across markets. However, the combination of historically low interest rates, a surge in demand for single-family homes, and constrained inventory turned this challenging period into an investor’s paradise. The housing market quickly rebounded, defying expectations and delivering extraordinary opportunities for those positioned to take advantage of the conditions.

Today, more than five years after the start of the pandemic, the real estate market continues to feel the ripple effects of the monetary policies enacted during that time. The Federal Reserve’s rapid rate hikes to combat inflation have drastically altered the borrowing landscape, influencing 10-year treasury rates up and subsequently raising mortgage rates to 7.04% for a 30-year fixed loan today (January 18, 2025), and reducing affordability for both homeowners and investors. While home price growth has slowed in many areas, it remains positive nationally, with existing single-family home sales increasing 7.4% year-over-year in November 2024.

Looking ahead to 2025, the U.S. economy appears to be on track for a soft landing, with the real estate market poised for growth despite its confusing and contradictory conditions. Key factors, such as inelastic interest rates, expected price growth, lowered consumer confidence, speculative inflation, rising unemployment, and the fiscal policies introduced by the newly elected president, Donald Trump, paint a nuanced picture of the opportunities and challenges investors face. Investors will be “taking a shot in the dark” when deciding to invest in the market today. Real estate and the macroeconomic cycle in the long run remain highly correlated, much like the historical relationship between unemployment rates and average vacancy rates (excluding pandemic-related anomalies).

In 2025, we can expect declining vacancy rates, due to the expansion of the real estate supply post pandemic and increased tenant demand due to sustained demand for rental housing and economic growth. However, with the 10-year Treasury yield likely to remain above 4% due to persistent budget deficits and inflation concerns, mortgage rates will remain sticky keeping borrowing costs high.

For single-family home investors, whether they are new entrants to the market or seasoned professionals looking to expand their portfolios, understanding macroeconomic dynamics and the real estate market cycle is essential. These insights not only inform whether it’s a good time to invest but also help define the appropriate investment strategy, such as a buy-and-hold approach for long-term cash flow or fix-and-flip for short-term gains. Additionally, it’s critical to recognize the significant regional differences in real estate markets. Conditions vary between the Northeast, Midwest, South, and West, and even from city to city within the same state.

This analysis focuses on a single-family property in Waco, Texas, a market that exemplifies growth and resilience. Waco enjoys steady population increases, a high quality of life, affordable housing, and diverse industries, including manufacturing, education, healthcare, and technology. Recent developments, such as the opening of a major Amazon distribution center, alongside large employers like Sanderson Farms and Mars Wrigley Confectionery (which produces North America’s Starbursts and most Skittles), underscore the city’s strong economic foundation.

This case study serves as a practical guide to real estate investment analysis, demonstrating how to critically assess a property’s financial viability while considering the broader economic environment. Rather than drawing broad conclusions from a single property, this analysis emphasizes the importance of data-driven decision-making, market evaluation, and financial forecasting in shaping investment outcomes. By examining key financial metrics, the goal is not simply to determine whether a property is a good investment in isolation but to understand the analytical tools necessary to navigate an ever-changing real estate landscape.

Property Overview:

This analysis centers on 712 Dickens Drive, a 1,510-square-foot single-family home in Waco, Texas, a city that epitomizes economic growth and stability in today’s evolving real estate market. The property was listed on Zillow January 16th, 2025. Built in 1963, the property features 3 bedrooms and 2 bathrooms and is listed at a purchase price of $175,000. Located in the Westminster neighborhood, the property offers a combination of affordability and investment potential, aligning with the broader trends seen in Waco’s housing market.

The property is expected to generate $1,850/month in rental income when compared to similar properties in the same area. However, we will be safe and assume a $1,750/ month rent, which still satisfies the 1% rule (monthly rent should be greater than or equal to 1% of the property’s purchase price).

Net Operating Income (NOI) measures the property’s profitability after operating expenses but before debt, tax, depreciation & amortization. Like how EBITA is used to evaluate how efficiently a company is operating, NOI can do the same for income producing properties. It can be a method in determining the risk, while also determining the initial value of a particular investment. However, future cash flow and growth in expenses can be difficult, making NOI a non-clear indicator for the performance of a property over time. It can be lucrative to compare NOI of a particular property in your portfolio each year.

The Capitalization Rate (Cap Rate) is a metric used to evaluate the return on an investment property based on its NOI relative to the purchase price. It represents a quick and easy assessment whether a property meets their return expectations. The capitalization rate demonstrates an insensitivity to financing costs, as it evaluates a property’s profitability without considering the impact of high or low mortgage rates. This decoupling from debt service can obscure the true financial burden borne by the investor. Other factors such as location, likely hood of weather hazards, safety rating of the neighborhood, all of which contribute to the overall risk and potential returns of the investment that the cap rate doesn’t capture.

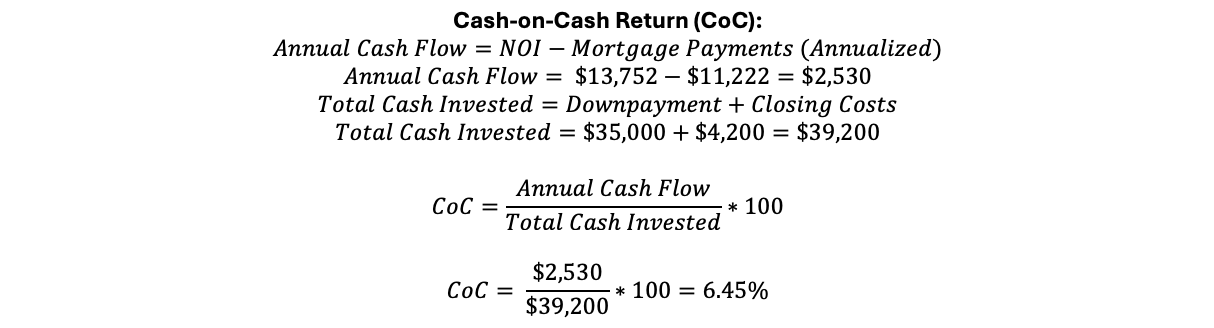

Cash-on-cash return is an excellent metric for evaluating immediate returns. Unlike NOI and the cap rate, it incorporates debt into the calculation, giving investors a clearer picture of their “day one” returns. However, determining cash-on-cash return over time relies on the assumption that the market may readjust for various reasons. Additionally, it does not account for property appreciation, making cash-on-cash return a primarily short-term metric for assessing investment performance.

Okay, so we have accomplished the net operating income, the cap rate, and cash-on-cash return on this particular investment property, we can analyze the figures.

The NOI of $13,752 is a strong indicator of the property’s profitability, showcasing its ability to generate income after covering operating expenses. This figure reflects operational efficiency and provides a basis for comparing similar properties. While positive, it assumes stable expenses and consistent rental income, which may not reflect reality. Future risks, such as unexpected maintenance or vacancy, could erode NOI, and it does not consider debt servicing or taxes. Thus, while the NOI appears promising, it must be contextualized within broader market dynamics and risk factors.

A cap rate of 7.9% is generally considered excellent, as it sits comfortably within the “good” range of 5%-10% and exceeds the safe threshold of 4%. For investors looking to balance risk and reward, this figure is a positive indicator of the property’s income-generating potential relative to its purchase price. However, it is important to note that a higher cap rate often signals increased risk, such as location-related concerns, tenant reliability, or market volatility. In this case, while the cap rate suggests strong returns, it could also reflect underlying risks not immediately evident in the financials, such as potential maintenance issues, safety concerns, or shifts in neighborhood desirability.

At the same time, the 7.9% cap rate may also indicate heightened demand for the property. Increased attention could drive competition and potentially boost prices in the area, which is favorable for long-term appreciation. However, it is crucial to acknowledge that the cap rate, by nature, does not account for financing costs, macroeconomic conditions, or broader qualitative factors like tenant demand stability. As such, while the cap rate is an excellent starting point, it should not be relied upon in isolation for investment decisions.

The CoC Return of 6.5% provides a solid picture of immediate, levered returns, indicating that the property delivers consistent cash flow relative to the cash invested. This return alone isn’t impressive. The S&P500 in 2023 and 2024 produced returns of 24.2% and 23.3% respectively. But it is important to note that the cash-on-cash return is the immediate return on invested capital and does not represent the return expected over the lifetime of a rent producing property.

To determine the overall return the property can generate over a simple 5-year buy-hold-sell period, we calculate the Internal Rate of Return (IRR). However, this calculation requires a few key assumptions:

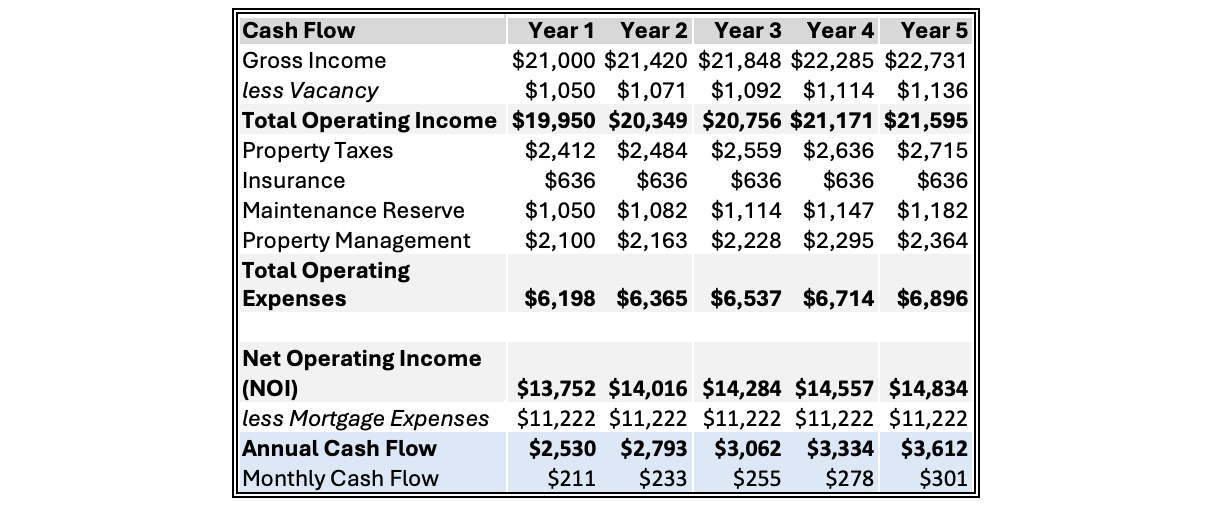

IRR is based on the Net Present Value (NPV) equation, as IRR is the discount rate (r) that makes the NPV of all future cash flows equal to zero. It considers the time value of money and provides a rate of return for the timing of cash flow. In the equation, we recognize as cash flow at time , as time period (in years), and as number of time periods. Below is the first 5 years expected cash flow.

We can calculate the cashflow based on the assumptions for income and expense appreciation. Here we see how annual cashflow gradually increases as rent increases. To calculate IRR, we still need to estimate the equity at time of sale, we can do this with estimating the principal on the loan, and yearly appreciation. Below is the first 5 years of the amortization schedule for the loan on this property.

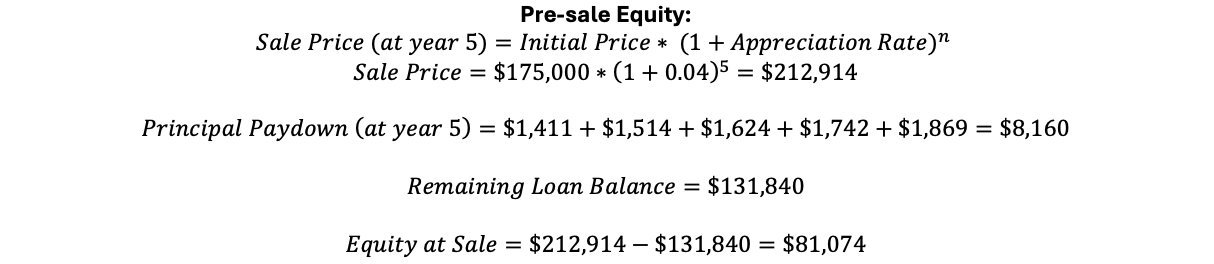

Over the 5-year period, a total of $8,160 is paid toward the principal, adding to the equity in property. As mortgage rates increase, a larger portion of the monthly payment will go towards interest. As in the case with this loan, a substantial part of the payment goes towards interest. We estimate an annual appreciation rate of 4% and have updated the cash flow table below to reflect appreciation, and principal paydown.

With the calculation of the unrealized gain through equity, it becomes clear the growth power that an investment can hold. It only really takes 3 years and several months to make back the capital spent in the initial investment. Additionally, we learn the growth of cash flow, however, it is purely based on assumption and does not take into consideration potential unexpected expenses. Continuing the calculations for IRR, we must now calculate the equity on the property at time of sale.

$81,074 is the total equity earned on the property at time of sale. This value does not take into consideration closing costs.

This means that total net expected profit after closing on the Waco property at the end of year 5 should be $64,041. Finally, with all the necessary data acquired, the IRR can be calculated.

Solving for the discount rate (r) we get an IRR of 16.7%. This means that over the 5-year investment period, the property is expected to generate an average annual return of 16.7%, considering both cash flow and appreciation. While an IRR of 16.7% is lower than the annual return seen by the S&P500 with 24.3% in 2023 and 23.3% in 2024 in the wake of the economic growth provoked by COVID-19, the 5-year return of the S&P was 15.4 %. Slightly less than the return generated by the analyzed property.

A seasoned stock market investor might not be impressed by a mere 1.3% higher return, especially considering the effort required to acquire, manage, and maintain a real estate investment. Securities, by contrast, typically offer a far more passive approach. That said, real estate provides an alternative investment strategy that can generate comparable or even higher long-term returns, while offering a tangible, income-generating asset that instills greater confidence in investors.

Risk is an inherent part of any investment. While real estate requires active management, it can serve as a hedge against stock market volatility. For instance, in 2022, the S&P 500 delivered a -19.4% return, reinforcing the unpredictability of equities. This highlights a key principle, higher returns come with higher risk. While neither asset class is risk-free, real estate offers income stability, appreciation potential, and diversification, making it a compelling investment alternative in a well-balanced portfolio.

Continuing the calculation for IRR the same way but over 10 years and 30 years, we get 17.5% and 14.4% respectively. While US stock market return for the last 10 and 30 years are 13.3% and 10.9%. The declining IRR of the property implies there is a point where the investor can maximize return considering diminishing returns and the time value of money. While the IRR for the US markets are largely due to market volatility captured year over year. It is important to note that comparing real estate investing to the S&P as the key vessel for security investment is superficial. There are many other methods of investment in the realm of securities that can exceed returns of the S&P, however, in this case, the S&P can be a useful metric when comparing to the investment of physical property.

Changing the Data:

What if the mortgage rates dropped/ rose dramatically? What if we managed to secure the property for a lower price? Or maybe paid substantially more in the downpayment? And what if the average vacancies grew dramatically? What if the property needed sizeable and abrupt repairs? These are all questions an investor should answer before investing in a property to ensure the financial risk involved in the property is understood.

If the property price rose to $200,000 from $175,000, the investment would be much less captivating. In fact, if the price rose that high, the cash on cash would be 2.1% and reflects an unattractive short term return rate.

If the mortgage rates dropped to 4.0%, then the cap rate rises to 8.5% and 5-Yr IRR rises to an astounding 25.0%.

If rent doesn’t grow, then IRR slowly declines after year 10 as costs rise but income remains constant.

Real estate investing is not static, market conditions, interest rates, and property expenses fluctuate, often in unpredictable ways. Investors must be realistic and flexible when analyzing a deal, understanding that data-driven projections are only as good as the assumptions behind them. A shift in mortgage rates, purchase price, or rental growth can drastically alter an investment’s profitability.

Investment Analysis Conclusion:

Ultimately, this analysis highlights the importance of strategic decision-making in real estate investing. While the property presents strong income potential with a 7.9% cap rate, 6.5% cash-on-cash return, and a 5-year IRR of 16.7%, these figures are not static. Market conditions, financing terms, and property-specific risks all influence the long-term performance of the investment.

Real estate offers tangible asset security, steady appreciation, and leverage benefits, but it also requires active management and careful financial planning. Compared to the stock market, which provides higher short-term liquidity but greater volatility, real estate delivers consistent cash flow and long-term stability. However, as the declining IRR over time suggests, there is an optimal holding period where investors can maximize returns before diminishing leverage benefits set in.

The key takeaway is that real estate investing demands adaptability. Investors must account for changing variables, stress-test different scenarios, and remain realistic about both potential gains and risks. While no investment is risk-free, a well-researched, data-driven strategy can help maximize returns, mitigate uncertainty, and build long-term wealth in an ever-evolving market.

Bibliography:

“712 Dickens Dr, Waco, TX 76710: MLS #227512.” Zillow,www.zillow.com/homedetails/712Dickens-Dr-Waco-TX-76710/52104037_zpid/. Accessed 4 Feb. 2025.

Beck, Rae Hartley. “How Did Covid-19 Affect the Housing Market?” Edited by Michele Petry, Bankrate, 23 Aug. 2023, www.bankrate.com/real-estate/covid-impact-on-the-housing-market/.

CBRE. “2025 U.S. Real Estate Market Outlook.” CBRE.Com, mktgdocs.cbre.com/2299/2365fedf-2f92-4e93-aac8-909a56d3a7f9-148392495.pdf. Accessed 4 Feb. 2025.

“Current US Inflation Rates: 2000-2025.” US Inflation Calculator | Easily Calculate How the Buying Power of the U.S. Dollar Has Changed from 1913 to 2023. Get Inflation Rates and U.S. Inflation News., 15 Jan. 2025, www.usinflationcalculator.com/inflation/current-inflation-rates/.

Hoover, Carl. “What’s the Job Market like in Waco, TX?” US News, realestate.usnews.com/places/texas/waco/jobs. Accessed 4 Feb. 2025.

“How to Buy Investment Property in Waco TX in 2024.” Longleaf Lending, 22 Jan. 2024, longleaflending.com/waco-tx-real-estate-guide.

Mitchell, Cory. “Investors’ Guide to Real Estate Market Cycles.” TradeThatSwing, 6 Jan. 2025, tradethatswing.com/average-historical-stock-market-returns-for-sp-500-5-year-up-to-150-year-averages/#:~:text=Stock%20Market%20Average%20Yearly%20Return%20for%20the%20Last%205%20Years,This%20assumes%20dividends%20are%20reinvested.

NATIONAL ASSOCIATION OF REALTORS®. Existing Single Family Home Sales, www.nar.realtor/sites/default/files/2024-12/ehs-11-2024-single-family-only-2024-12-19.pdf. Accessed 4 Feb. 2025.

“News Release.” Gross Domestic Product (Third Estimate), Corporate Profits (Revised Estimate), and GDP by Industry, Third Quarter 2024 | U.S. Bureau of Economic Analysis (BEA), www.bea.gov/news/2024/gross-domestic-product-third-estimate-corporate-profits-revised-estimate-and-gdp-1. Accessed 4 Feb. 2025.

Robertson, Colin. “The Reason Mortgage Rates Jumped after the Fed Rate Cut.” The Truth About Mortgage, 1 Feb. 2025, www.thetruthaboutmortgage.com/the-reason-mortgage-rates-jumped-after-the-fed-rate-cut/.

Santarelli, Marco. “Today’s Mortgage Rates Rise to 6.7% - December 20, 2024 Update.” Norada Real Estate Investments, 20 Dec. 2024, www.noradarealestate.com/blog/todays-mortgage-rates-on-the-rise-6.7-percent-as-of-december-20-2024/.

“Unemployment Rate.” FRED, 10 Jan. 2025, fred.stlouisfed.org/series/UNRATE.

“United States Fed Funds Interest Rate.” United States Fed Funds Interest Rate, tradingeconomics.com/united-states/interest-rate. Accessed 4 Feb. 2025.

“Waco, TX 2025 Housing Market | Realtor.Com®.” Realtor.Com, www.realtor.com/realestateandhomes-search/Waco_TX/overview. Accessed 4 Feb. 2025.

Woodman, Carmel. “Investors’ Guide to Real Estate Market Cycles.” New Silver, 11 Dec. 2024, newsilver.com/the-lender/real-estate-market-cycles/#:~:text=created%20more%20unpredictability.-,What%20stage%20of%20the%20Real%20Estate%20Cycle%20are%20we%20in,estate%20market%20may%20be%20different.